A prolonged closure of the Strait of Hormuz poses the single greatest threat to global energy markets in decades, according to a new Horizons report from Wood Mackenzie, Strait Talking: Iran War Scenarios and the Future of Energy.

More than 11 million barrels per day (b/d) of Gulf crude and condensate production is currently curtailed.

Meanwhile, over 80 million tonnes per annum (Mtpa) of LNG supply, equivalent to around 20% of global supply, remains inaccessible to global markets.

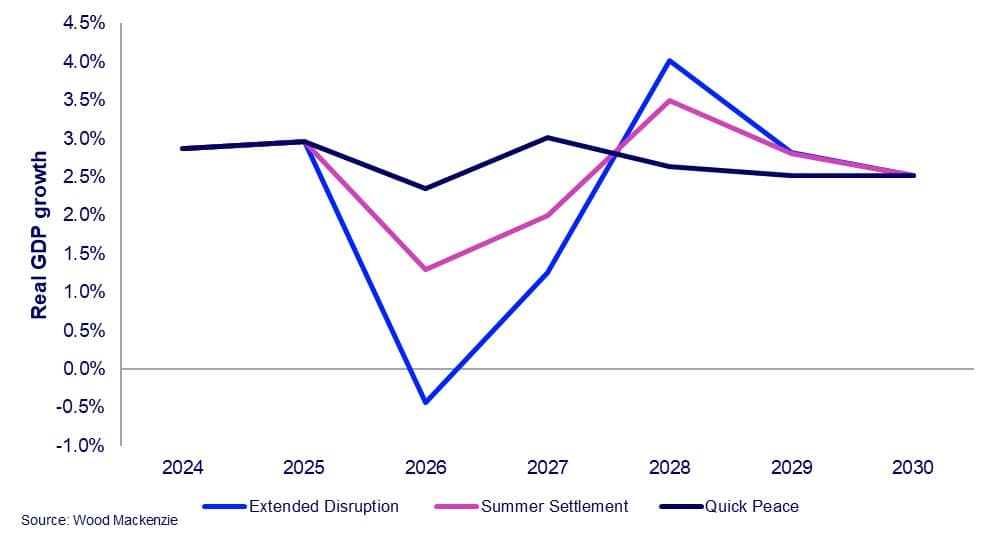

In its new report, Wood Mackenzie has shared three distinct scenarios: Quick Peace, Summer Settlement and Extended Disruption.

Each scenario offers a different timeline for ending the conflict and reopening the Strait and assesses the potential impact on oil and gas supply, prices, energy demand and the broader global economy.

“The Strait of Hormuz is the most critical chokepoint in global energy markets, and a prolonged closure would become far more than an energy crisis,” said Peter Martin, head of economics at Wood Mackenzie. “The longer disruption persists, the greater the impact on energy prices, industrial activity, trade flows and global economic growth.”

Under the most optimistic ‘Quick Peace’ scenario, a workable peace agreement is reached in the near term, and the Strait reopens by June. The global economy broadly returns to its pre-war trajectory by Q4 2026.

Crude prices fall sharply following a deal, with Dated Brent easing to around US$80/bbl by end-2026 and declining further to US$65/bbl in 2027 as the oil market returns to oversupply.Global GDP growth slows from 3% in 2025 to 2.3% in 2026, with a recession limited to the Middle East. The global economy broadly returns to its pre-conflict trajectory by Q4 2026.

The ‘Summer Settlement’ scenario assumes the ceasefire holds but negotiations extend into late summer, with the Strait remaining largely closed until September.

Oil and LNG supply shortages persist through Q3 2026, driving a shallow global recession in H2 2026. Global GDP growth falls below 2% in 2026, resulting in modest yet permanent economic scarring compared to the pre-war baseline.

Under the most severe scenario, the Strait remains largely closed through the end of 2026, with recurring tensions triggering periods of renewed conflict and sustained supply disruption.

Wood Mackenzie’s analysis indicates that Brent crude prices could approach US$200/bbl by the end of 2026, despite global oil demand falling by 6 million b/d year-on-year in H2 2026.

More than 11 million b/d of crude and condensate production remains shut in, and global oil inventories continue to decline. Diesel and jet fuel prices could rise towards US$300/bbl in major refining centres by year’s end.

The global economy could contract by as much as 0.4% in 2026, marking the third global recession this century, with significant economic scarring.

Oil- and gas-importing countries could intensify efforts to reduce their import dependence by aggressively accelerating electrification.

The regional economic impact would be severe and uneven. The Middle East could see GDP contract by 10.7% in 2026, while the EU27 GDP declines by 1.5% in 2026 and 0.5% in 2027. US GDP growth would fall below 1% in both years, while China’s GDP growth slows to 3% in 2026.

“The long-term outlook points to structurally weaker oil prices than in our pre-conflict base case if importing countries accelerate efforts to reduce oil dependence,” said Alan Gelder, senior vice president for refining, chemicals & oil markets at Wood Mackenzie.

“If electrification advances more aggressively and oil imports are displaced, this will add further downward pressure on prices, with Brent potentially trending US$10/bbl lower than the quick peace scenario in the medium/long-term.

“This outlook is, however, challenged by both the pace of the energy transition and higher energy costs for oil-importing economies that seek to reduce reliance on hydrocarbons.”

The report finds that the global LNG market faces varying degrees of disruption across the three scenarios.

Even under Quick Peace, LNG markets remain tight through summer 2027 as Gulf export facilities recover gradually and construction delays slow the next wave of supply growth from the region.

A major global LNG expansion remains underway, with supply expected to increase by around 200 Mtpa by 2031, roughly 50% above current levels. The anticipated oversupply is delayed rather than eliminated.

Wood Mackenzie expects US LNG cargo cancellations may eventually be required to rebalance the market, with European TTF prices in the early 2030s almost half of 2026 levels of around US$14/mmbtu. Prices then stage a recovery through to 2035.

Under the Extended Disruption scenario, the market outlook becomes significantly more severe.

Some of the Gulf region’s existing 85 Mtpa of LNG supply could be permanently lost, while around 75 Mtpa of capacity currently under construction faces multi-year delays. As a result, global LNG supply could be on average 70 Mtpa lower than expected before the conflict.

“Persistent supply uncertainty would accelerate efforts to diversify away from imported LNG, supporting coal resilience and faster growth in renewables and electrification across Asia and Europe” said Massimo Di Odoardo, vice president of gas and LNG research at Wood Mackenzie. “LNG prices would remain elevated through to 2030, supporting investments in new LNG outside the Gulf, but lower long-term demand would risk undermining the industry’s future perspectives.”

Beyond the immediate supply shock, Wood Mackenzie suggests that a prolonged conflict could accelerate structural changes across global energy markets.

Even after the Strait reopens, intermittent disruptions could continue to reinforce the geopolitical risk associated with both oil and LNG trade flows, creating a more volatile pricing environment and increasing pressure on import-dependent economies to strengthen energy security.

In the Extended Disruption scenario, countries across Europe and Asia intensify efforts to reduce hydrocarbon dependence through accelerated electrification. At the same time, resource-rich producers outside the Gulf, including US LNG exporters, benefit from growing demand for supply diversification.

The report also highlights the increasing strategic importance of critical minerals supply chains as faster electrification and renewable deployment drive stronger demand for metals needed across clean energy technologies.

“The consequences of an extended disruption would extend well beyond energy markets,” Martin concluded. “It would test the resilience of global trade, industrial supply chains and economic growth simultaneously, reinforcing the urgency of achieving a resolution.”

Leave a Comment