You have heard the horror stories: an owner waits three months for an SBA loan, then a surprise “packaging fee” adds thousands at closing.

In this article you will find a ranking of 25 active SBA lenders on speed, true up-front costs, interest rates, annual deal volume, and customer reviews. The result is a data-driven Top 6 for 2026 — built to get capital in your account weeks faster than the 60–90-day norm.

SBA loan programs at a glance

SBA lenders work across three core programs, each built for a different cash-flow puzzle.

The 7(a) loan is the Swiss-army knife of government-backed capital. Use the money for almost anything — equipment, refinancing, or real estate — with terms up to 25 years on property deals.

The 504 loan partners a bank with a Certified Development Company. The bank funds half, the CDC up to 40 percent at low fixed rates, and you cover the rest. Real estate or heavy machinery serves as collateral, so rates stay competitive.

SBA Express loans and Microloans round out the lineup. Express tops out at $500k and often closes in 30–60 days. Microloans, under $50k, flow through nonprofit intermediaries and suit startups that just need a gentle push.

| Program | Max amount | Typical use | Max term | Speed |

| 7(a) | $5 million | Working capital, refinancing, real estate, buy a business | Up to 25 yrs | 60–90 days |

| 504 | $5.5 million (CDC portion) | Owner-occupied real estate, heavy equipment | 10–25 yrs | 45–75 days |

| Express | $500k | Short-term or bridge needs | 7–10 yrs | 30–60 days |

| Microloan | $50k | Startup supplies, working capital | 6 yrs | 30–45 days |

A lender that excels at Express loans may crawl on a 504 deal, and the reverse is also true. This article ranks the field below, flagging the specialty each institution masters.

How winners were selected

Each lender was scored on five borrower-focused metrics with clear weights:

- Speed (30%) — Days from complete application to funding. Top lenders fund in about six weeks; laggards stretch past three months.

- Up-front fees (25%) — Packaging, origination, and the reinstated guarantee fee. The ranker counted every dollar that leaves your account.

- Interest rates (20%) — A one-point bump on a 10-year, $1 million loan adds roughly $58,000 in payments.

- SBA lending volume (15%) — High-volume banks hold Preferred Lender status, which shortens approval cycles.

- Customer reputation (10%) — BBB, Trustpilot, and community forums to spot praise or pain.

These metrics were converted to a 0–10 score, multiplied by its weight, and lined up the totals.

The six leading SBA lenders of 2026

1. Lendio: fastest route to multiple offers

Lendio is not a bank; it is a marketplace that sends one application to more than 75 SBA-approved partners and returns side-by-side quotes in minutes. Turning days of comparison shopping into clicks gives it the highest speed score in the study.

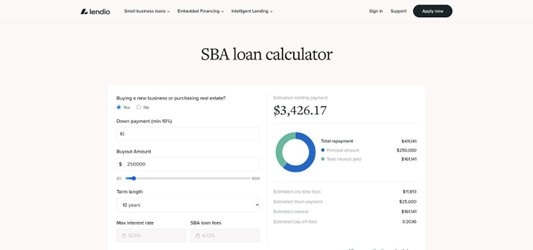

Because Lendio earns referral fees, it waives the packaging charges many brokers add at closing, and its free SBA loan calculator lets you preview payments for any loan amount and term.

Lendio

Screenshot of Lendio SBA loan calculator marketplace page.

When to choose it: you need around $350k for inventory before the holiday rush and do not have time to contact ten banks. Submit one application, compare offers, and let the quickest lender win. Watch-out: after you pick a partner, underwriting speed and final pricing depend on the bank behind the curtain.

2. Live Oak Bank: biggest SBA checkbook in the game

Live Oak funded nearly two billion dollars in 7(a) volume last year — more than some regional banks handle in a decade. That scale produces seasoned underwriting teams and Preferred Lender Authority, trimming weeks from approval. Dedicated industry pods match you with loan officers who know your vertical (veterinary, self-storage, pharmacy, and more), so fewer clarifying emails mean faster credit decisions.

Pricing stays transparent. Live Oak posts its SBA rate matrix online and seldom adds discretionary origination fees. You still cover the standard guarantee charge, but there is no surprise broker markup at closing.

The trade-off is strict underwriting. Expect a 650-plus credit score and two consecutive profitable years. Choose Live Oak when you are pursuing a seven-figure loan to buy real estate or a cash-flowing business and want a lender with deep pockets and niche expertise.

3. Huntington National Bank: Midwest workhorse with a heart for Main Street

Huntington leads the nation in number of SBA 7(a) loans, proof that it is comfortable writing smaller checks many megabanks overlook. If you need a $200k remodel or a quick Express line, Huntington’s blend of production muscle and hometown service stands out.

The Lift Local program waives origination fees and lowers down payments for women, minority, and veteran owners, cutting thousands from day-one costs. Combined with Preferred Lender Authority, approvals often land inside six weeks.

Limits start with geography. Branch coverage centers on the Midwest and parts of the Mid-Atlantic. Choose Huntington when you value face-to-face guidance, want fee relief, and operate inside its footprint.

4. Celtic Bank: online speed demon for bigger borrowers

Celtic Bank operates almost entirely in the cloud. Independent audits place its average SBA 7(a) closing at about 14 to 16 days for loans over $1 million — far faster than the six-week industry median. A lean underwriting team focuses on larger tickets, with analysts reviewing tax returns and comps in parallel.

Borrowers also praise the “Celtic Advantage” line of credit, which blends SBA Express flexibility with term-loan pricing. You do pay for the speed: Celtic adds modest origination fees and often prices near the top of the SBA rate band. Choose Celtic when time is critical, your request exceeds seven figures, and a few extra basis points are worth a timeline that protects a contract.

5. Lendistry SBLC: mission-driven speed for underserved borrowers

If big banks have sidelined you for being “too new” or “too small,” Lendistry offers another path. The fintech, structured as a nonprofit Small Business Lending Company, focuses on minority, veteran, and low-income owners.

Lendistry ranks among the five fastest SBA Express funders, wiring cash about seven business days after credit approval. Costs stay reasonable — you still pay the SBA guarantee fee, but Lendistry skips broker packaging charges. Interest hovers near 12 percent, slightly above big-bank rates yet competitive once every line item is tallied.

Loans top out near $500k, and the company does not offer deposit accounts. Choose Lendistry when purpose matters as much as capital and you need quick funds without the premium many fintechs charge.

6. BayFirst National Bank: lightning cash for sub-$500k needs

BayFirst’s sweet spot is loans under $500k — the size many community banks push to the back of the queue. Independent trackers list BayFirst funding 7(a) loans in as little as six to eight business days when the file is clean, faster than some lenders issue a term sheet. An “Express Core” team pre-underwrites files the same day they arrive.

Pricing runs higher than a big-bank term loan; expect double-digit variable rates tied to Prime. Total fees stay low, though — BayFirst rarely adds an origination premium. Average loan size sits near $166k, and the footprint is Florida-centric. Choose BayFirst when you need a five- or six-figure check inside two weeks.

How the top lenders stack up on speed and cost

| Lender | Avg. days to fund | Typical APR range | Up-front fees |

| Lendio (network) | 35–45 | 10.5–12.0% | $0 packaging |

| Live Oak Bank | 40–50 | 9.0–10.5% | 0.5% origination |

| Huntington Bank | 45–60 | 10.0–11.5% | Waived for Lift Local |

| Celtic Bank | 14–16 | 10.5–12.5% | 1.0% origination |

| Lendistry SBLC | 30–35 | 11.5–13.0% | $0 packaging |

| BayFirst Bank | 6–8 | 12.0–13.5% | $0 origination |

Celtic’s two-week average for seven-figure loans handily beats the field, though the rate nudges higher. BayFirst moves even faster, but you pay in double-digit interest. Live Oak balances volume and price, funding nearly two billion dollars a year while keeping rates below 11 percent.

Choosing the right SBA lender for your situation

Start with timing. If a seller gives you 30 days to close, speed rules — BayFirst, Celtic, and Lendistry specialize in quick turnarounds. If the schedule is relaxed and every basis point matters, Live Oak can save meaningful interest over a 10-year term.

Next, deal size. Sub-$500k requests rarely excite big banks, so files linger; BayFirst and Huntington fill that gap. For a multimillion-dollar acquisition, look to Live Oak’s industry pods or Celtic’s large-loan focus.

Finally, check hidden costs. A lender marketing an eight-percent rate but adding a 1.5 percent origination fee can end up pricier than a 10 percent offer with no extras. Request a full closing-cost worksheet — guarantee fee, packaging, appraisal, and environmental reports — before locking in an APR.

Frequently asked questions

How long does an SBA loan take?

Preferred lenders with streamlined authority close a complete 7(a) file in 45 days or less. Standard-processing banks often need 60–90 days because the SBA must sign off at several checkpoints.

What hidden fees should I watch for?

Packaging or application charges lead the list. They cover lender prep work and range from zero dollars at Lendio or Lendistry to one percent of the loan at some banks. Expect third-party costs like appraisals, environmental reports, and attorney closings as well.

Can I apply with several lenders at once?

Yes. The SBA assigns a loan number only when a lender submits your file, so you may compare offers until you sign an intent-to-proceed letter. Marketplaces such as Lendio simplify this step by routing one application to multiple partners.

Why do SBA interest rates differ if the program sets a cap?

The cap is a ceiling, not a mandate. Each lender adds a margin to the Prime rate based on risk, loan size, and funding costs. Live Oak’s efficient model lets it price below peers, while some fintech lenders charge more to cover higher capital expenses.

The above information does not constitute any form of advice or recommendation by London Loves Business and is not intended to be relied upon by users in making (or refraining from making) any finance decisions. Appropriate independent advice should be obtained before making any such decision. London Loves Business bears no responsibility for any gains or losses.

Leave a Comment