The lessons of the 1970s are being forgotten

All politicians agree that they can’t pick winners.

Labour’s Chuka Umunna agrees. LibDem Vince Cable agrees. Even the most left-leaning Tory in government, Ken Clarke, agrees.

Picking winners in business is what we did in the 1970s, when the government lost eye-watering sums on British Leyland and ICL.

It’s what the statist economies of the Iron Curtain did. They ended up needing electric fences and sniffer dogs to stop their people from fleeing to free-market nations.

Saying you want to use taxpayer money to promote a few selected firms is up there with claiming the Rotary Club shot JFK or that the Pentavaret rules the United Nations.

Until now.

Suddenly politicians want to pick winners again.

The Olympic Games is one source of inspiration.

“You can’t pick winners. Tell that to Bradley, Jessica or Mo, all supported by targeted funding. Markets always trump planning, they say. Well look at the Olympic Park, the result of years of careful planning and public investment.”

That’s Brendan Barber in his final speech to the TUC.

The economics editor of The Guardian, Aditya Chakrabortty, is saying the same thing: “The entire Westminister establishment has spent decades rubbishing the notion of picking winners, of explicit state intervention in industry or of worrying who owns British assets. Apply this laissez-faire philosophy to British sport, and by now Jessica Ennis would have been flogged off to the Qataris.”

“Really, there’s something wrong with picking winners? Tell that to Bradley Wiggins.”

Okay, you might expect that rhetoric from a trades unionist and a writer for a paper which loves to wind up its left-wing readership.

But Chuka Umunna, Labour’s suave shadow business secretary is endorsing the idea. He says, “we need a clear focus on the needs of individual sectors that can drive our future success. In this respect, I am intensely relaxed about picking sectors.”

Umunna is by reputation a centrist.

Vince Cable is making near identical speeches. Naturally, he avoids saying he wants to pick companies – that would be absurd! – but the noble doctor believes he can identify the right sectors to plough taxpayers money into.

In February business secretary Cable promised the oil sector support. He said state action would “re-energise” the sector to create “a different kind of economy”. Britain could not “just hope it happens naturally”. He promised he would not repeat the “cack-handed interventionalism of the 1960s and 1970s”. The car industry , he pointed out, had benefitted from the “explicit choices” of government support.

“Revolutionary technologies are often too risky, or simply too complex or resource intensive, for an individual company to make the necessary investment. For Government, there is a significant role here.”

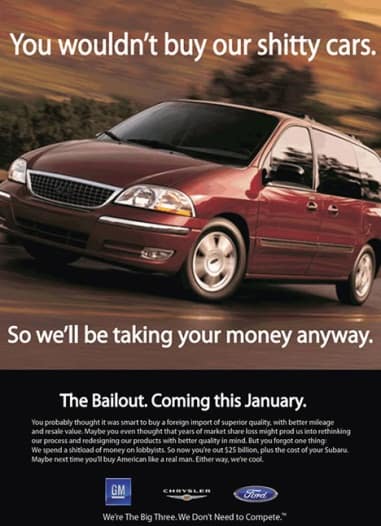

President Obama reversed decades of free-market thinking in when he bailout out US car-makers. The three firms still owe more than $50bn of the money they received in 2009. GM used the cash to produce more Chevvy Volts – one the industry’s worst selling models.

Obama said: “On the day I took office, our auto industry was on the verge of collapse. Some even said we should let it die. With a million jobs at stake, I refused to let that happen,” the president said. “Today, General Motors is back on top as the world’s No. 1 automaker.”

The reaction? Opposition to the move was neatly summed up by this spoof advert.

This isn’t off-message. This is Coalition policy.

Just look at the raft of projects David Cameron has authorised.

In December last year the prime minister announced a £180m Catalyst fund for the pharmaceutical industry. The money is to be used to fund early stage research into molecules and other pharma technologies.

He launched the Green Investment Bank to fund green schemes. It cannot borrow money until the national debt falls as a percentage of GDP, scheduled to be 2015. Until then it has £3bn to invest via its London and Edinburgh offices.

In July a £120m package for the aerospace industry was announced at the Farnborough Airshow, including £40m for research into low-carbon engines led by Rolls-Royce. Cable said the UK had been “inhibited” from picking winners, but it was a “no-brainer” to back British aerospace, which is the world’s second largest behind the US.

Even George Osborne is on board, demanding a British Investment Bank.

And the reaction from industry leaders? Near unanimous approval.

An investigation by PA Consulting involving input from 112 private sector firms including Nokia, Proctor & Gamble, Kraft Foods and Nestle revealed strong support for state-support for sectors, if not for picking individual firms.

Tory MP George Freeman, who worked with PA Consulting on the research, said: “This is not a call for a return to 1970s’ ‘Industrial Policy’ of ‘picking winners’ at a company level, subsidies or protectionism. It is about a new partnership approach with Government supporting business led, sector-specific strategies for key sectors and technologies in which Britain is globally competitive.”

The engineers association EEF is backing state intervention. EEF chief executive Tony Scuoler says the government should be “developing a range of alternatives to Bank finance” – namely the British Investment Bank mooted in various forms by all three major parties.

How about City grandees?

Sir John Parker, chairman of mining giant Anglo American, is a fan of a new industrial policy. He recently stated: “We are not picking winning companies, we are looking at sectors. They will create a pull for research and development programmes, for skills training and for joined-up thinking across government departments.”

He cited Bombardier, whose train building division has struggled lately. “If it was decided that train building is a sector we need to be in over the next 20 years and if you hit a hard spot, as Bombardier has, then you would want to look hard at finding ways to support it, to help it through the trough.” He added: “If you don’t have that, policymakers have to jump from rock to rock. It is this coherence that we need across government departments, in support of those chosen sectors.”

Okay, so the language is about picking sectors, not individual firms, but in the end we are talking about taxpayer cash being handed over to specific firms, either directly or through subsidies.

Perversely, the change comes at a time when Nordic

nations, allegedly models of social democratic industrial partnerships, are abandoning government meddling. When Saab needed a bailout to survive, the Swedish government refused. Saab fell.

When the Icelandic banks needed a bailout, the Icelandic government refused. Kaupthing and Glitnir collapsed. Analysis is increasingly favouring this action as the right one.

The lesson of history is that politicians come under huge pressure to intervene to help ailing firms, or companies in trendy industries or electorally sensitive locations. Resisting the siren call can be almost impossible.

Even the Iron Lady crumbled. In the early 1980s Margaret Thatcher paid for yet another bailout of British Leyland. In her diaries she justified the payout saying, “political realities had to be faced…BL had to be supported”.

She confessed:

“I knew that closure of the volume car business, with all that would mean for the West Midlands and the Oxford area, would not be politically acceptable to the Cabinet of the Party, at least in the short term. It would also be a huge cost to the Exchequer — perhaps not very different to the sort of sums BL was now seeking.”

If she – the staunchest opponent of bailouts in British history – could not control herself, what chance the politicians of today, who believe their use of taxpayer cash is vital?

More like this…

The case against a British Investment Bank

Billionaire John Caudwell throws economic challenge at government

Why is Ed Miliband more popular than ever? Here’s a handy explainer for you old people

Leave a Comment