The U.S. dollar index, which measures the strength of the dollar against a basket of major currencies including the euro, pound sterling, and Japanese yen, witnessed high volatility trading movements following the release of key U.S. inflation data.

It is now trading at 101.99 points. The index reflects market sentiment as the dollar lost some of its gains against most currencies but reached a one-month high against the Japanese yen during Thursday’s trading, partly influenced by energy costs.

The results of today’s Thursday data revealed a moderate increase in core inflation to 3.2% annually. The core rate excluding the food and energy sectors increased by 0.2% for July, in line with expectations, reflecting a yearly increase of 4.8%. Unemployment claims also rose, registering 248,000, significantly higher than anticipated.

It’s worth noting that recent fluctuations in U.S. Treasury yields and rising energy costs have deeply impacted the recently released inflation data. Considering key economic indicators and market sentiment, the trajectory of the U.S. dollar index is heavily reliant on Consumer Price Index (CPI) data, which showed a slowdown in inflation rates, increasing the likelihood of the Federal Reserve temporarily halting interest rate hikes, thus leading to a drop in the dollar index.

As a result, the loss in the U.S. dollar index expanded to 0.43%, accompanied by a collective decline in U.S. Treasury bond yields. The 10-year Treasury bond yields dropped by 0.47 to 3.993%. Gold managed to break the $1920 resistance level just moments after the positive inflation data announcement. The euro and pound sterling also rose against the dollar, reaching $1.1025 and $1.277 respectively.

European gas prices also increased due to potential strikes at Australian natural gas facilities, nearing their highest levels in two months. This is particularly pronounced as oil prices also rose to multi-month highs. There are increasing expectations of potential price changes by the European Central Bank amid the ongoing economic impacts of high energy costs.

In my opinion, the impact of the recently released U.S. Consumer Price Index data will likely be temporary, as the focus shifts to the upcoming U.S. Producer Price Index data on Friday. This index is favored by the Federal Reserve to accurately gauge inflation rates and the economy’s strength, which will significantly guide the Fed’s monetary direction in its upcoming meeting.

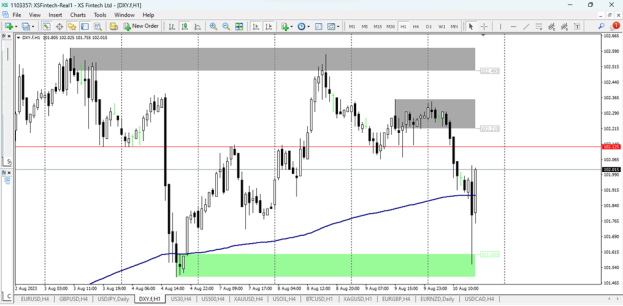

Source: The hourly chart for the U.S. Dollar Index prices – MetaTrader 4 platform from XS.com.

In the above chart, the price of the U.S. Dollar Index (DXY) reached 102.150 in the past four hours, which is marginally higher than the previous four-hour closing at 102.124, indicating a slight upward trend. This current price also sits above the 200-day moving average at 101.809, suggesting potential upward momentum. However, it is trading below the 50-day moving average at 102.302, indicating some resistance at this level.

The Relative Strength Index (RSI) indicates a somewhat weaker bullish momentum, as the signal line is below the midpoint level of 50 for the index. With the price below the short-term moving average and trading near the long-term moving average, the dollar index seems susceptible to a decline in the short term, followed by a potential recovery towards the 50-day moving average. This action could eventually shift the trend back upwards.

Leave a Comment