A new report reveals stark truths – and suggests how problems can be tackled

It’s all too easy to think of London as a hugely prosperous city.

And there’s no doubting that the capital is the most economically productive region in the country.

Anyone who has spent a day here can see there are some incredibly rich people who live and work in London.

The average house price in the capital is, after all, double the UK average and well over half a million pounds.

But London is a tale of two cities.

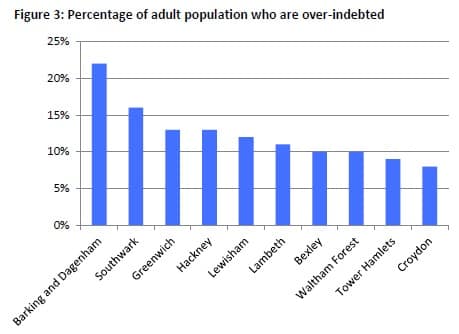

Some of our boroughs, such as Barking & Dagenham and Newham, have among the highest unemployment rates (2013 figures) and lowest income levels in the country.

There are many, many people living in the capital who simply cannot afford the sky-high costs of being based here.

A new report released today by the London Assembly’s Economy Committee reveals the extent of the problems many Londoners face.

“The numbers are worrying,” explains the committee’s chair, Baroness Jenny Jones AM. “Approximately half a million Londoners are currently over-indebted, or in financial difficulty.”

That’s around one in every 16 people living in London.

The report finds that the type of debt Londoners are struggling with has shifted in recent times. It’s not so much credit-card debt these days, but an inability to pay for fundamental costs such as utility bills and council tax.

Low-income households are also struggling to access mainstream credit and high-street credit, and so instead turn to expensive short-term credit options – payday loans and the like.

“An estimated 40,000 London households are using illegal moneylenders (loan sharks) each year,” the report finds.

This isn’t just a problem for the individuals and families in question, either.

“Importantly, the estimated social cost of London’s problem debt could be as much as £1.4bn, putting more of a burden on systems such as education and the NHS,” writes Jones.

Children are also “severely impacted by problem debt,” the report finds. “For example, 165,000 families (16%) in London are in arrears on household bills and credit commitments. This can place a severe strain on family wellbeing.”

These are the boroughs where debt is most an issue

What can be done?

Here are the recommendations from the committee:

Recommendation 1

Central government should ensure all London boroughs are adopting fair and transparent debt recovery procedures

Recommendation 2

London boroughs and London Councils should implement genuinely fair approaches to debt recovery and learn from each other about what works.

Recommendation 3

The Mayor should monitor whether London’s debt advice services are sufficiently resourced to deliver both crisis and preventive face-to-face debt advice. This monitoring would also include an assessment of the effectiveness of existing services and any areas of unmet need. This should be published on an annual basis in the Mayor’s annual equalities report.

The Mayor should then take further action if this monitoring identifies a shortfall in resources and/or service provision.

Recommendation 4

The Mayor should commission a ‘money advice week’, to promote debt advice and affordable credit options.

The Mayor would use this week to tackle stigma around financial difficulties and use Transport for London advertising sites to encourage uptake of debt advice services and promote affordable credit options.

The Mayor should take note of the evaluation of the Money Advice Service’s pilot of debt advice marketing to inform the development of this ‘money advice week’.

The Mayor should ensure that deterring illegal money lending is included within the scope of the ‘money advice week’.

Recommendation 5

The Mayor should take further action to promote savings options, such as credit unions, to a wide range of Londoners. This would support growth of the affordable credit market.

Recommendation 6

The Mayor should promote debt education for London’s children and young people, through the Personal Finance Education Group (PFEG). As part of this, the Mayor should incorporate lessons plans from the Illegal Money Lending Team to raise further awareness around illegal money lending.

Recommendation 7

The Money Advice Service should evaluate whether, and if so how, the piloting of debt advice marketing was successful in reaching hard-to-reach groups in London.

Read the full report by clicking on the attachment at the top-right of this article.

Let us know your thoughts in comments below.

London economic news, trends & insights

49 fascinating stats about women in the workplace

London pay gap falls for first time since crash

Related Files

Economy Committee – Personal Problem Debt Report

Leave a Comment