The basics (and the not-so-basics) of the new £75bn quantitative easing injection, and experts’ views

What is quantitative easing, and why is the government printing an extra £75bn of money?

Quantitative Easing (QE) is printing money. The Bank of England creates electronic money in a digital account. The money can then be used to buy assets. The economic theory is that this extra money can stimulate the economy, either by buying goods and services created in the private sector or by making it cheaper for government and corporations to borrow money.

What sort of figures are we talking about?

The new round of QE will see £75bn created, in addition to the £200bn created in the first round that started in March 2009.

What will this money be spent on?

The first round of QE was spent on buying government bonds (known as gilts). This made it cheaper for the government to borrow, and therefore cheaper for the private sector to borrow as a result.

There was speculation about what this round would be spent on. One possibility was the purchase of corporate bonds. In his speech to the Conservative Party conference this week, chancellor George Osborne said the government might buy billions of private sector bonds, particularly those of smaller companies. The issue became confused since small firms do not issue bonds.

The Bank of England has since announced that all the new money will be spent on gilts.

Why does QE help the economy?

The Bank of England will use its fresh cash to buy gilts. Some gilts are held by pension funds, insurance funds and other institutional investors. These institutions will then be motivated to invest the money from the sale elsewhere, triggering a rippling effect of transactions through the economy.

Meanwhile, banks may sell the gilts they hold to the Bank of England and use the money to lend to housing buyers and struggling businesses. The key thing is that the Bank of England’s purchasing of gilts pushes up the price, therefore lowering the yield. Lower yields reduce the cost of borrowing for businesses and households, helping with the economic recovery.

The Bank of England’s letter to the chancellor justifying the latest QE can be read here.

Does the money created through QE last forever?

No. In a few years time the money will be “unwound”. The taxpayer will need to sell the assets bought through QE, which will then be “automatically extinguished” – in other words, the money digitally created today will be one day be destroyed.

Is it ethical for the government to create money like this?

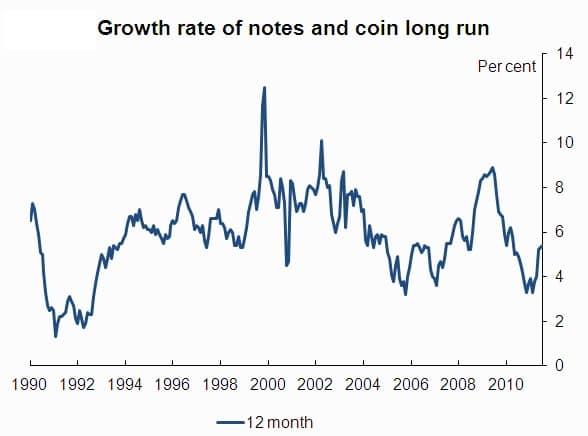

Big debate! But one small fact often gets overlooked: the government creates new money every year anyway, by expanding the amount of notes and coins (not accounting for the ongoing replacement of worn-out old notes). Here is the Bank of England’s data on the expansion of the total supply of notes and coins.

Source: Bank of England

The £75bn QE injection: the experts’ view

Alistair Darling, former Labour chancellor and who authorised the same policy in March 2009

Speaking yesterday morning on BBC Radio Four’s Today Programme ahead of the QE announcement:

“When I first authorised it, it was a completely different environment, it was just after the banking collapse in 2008. It came with a raft of measures to try and restore confidence and it worked. The economy started to grow at the end of 2009, it was growing until the middle of 2010, when, of course, growth stopped.

“And that’s the key point, the background against which the Bank of England is taking its decision today is one where the UK economy is stagnating, it has not grown for almost a year. It has to be done in such a way that makes sure the money actually leaves the bank vaults and gets out into the high street where it can be lent to businesses and to individuals. If that doesn’t happen, then it won’t have any effect at all.”

Andrew Sentance, former Bank of England Monetary Policy Committee member

Also speaking on yesterday’s Today Programme ahead or the announcement, Sentance gave three reasons why the Bank of England should be wary of quantitative easing:

1. “I don’t think the economic case is there. There are quite significant doubts about how effective it would be in the current climate. When the Bank of England used QE before, it had a significant effect because it came with other measures. It is very difficult really to isolate the effect of QE compared with other measures.”

2. “We have a high rate of inflation at the moment. It is 4.5 per cent and the Bank of England is meant to control inflation, and it would appear that it is trying to stimulate the economy when actually what is needed is to take measures to get inflation down.”

3. “Our ability to keep inflation low depends on the credibility that the Bank of England has as an independent institution. If the bank appears to be pushed around by politicians or the financial markets that is not really consistent with a credible, independent bank, which is committed to its low inflation target.”

The following are reactions to the announcement:

David Kern, Chief Economist at the British Chambers of Commerce (BCC):

“UK businesses welcome the MPC’s decision to increase the QE programme to £275 billion. In the face of the risks facing Britain’s recovery, it is important to make every effort to underpin business confidence and avoid a setback. However, higher QE on its own is not enough, and we urge the MPC to look at other radical methods. The Chancellor’s intention to use credit easing methods to help stimulate the flow of credit in the economy is a welcome initiative, but its implementation will take time and the MPC is better placed to move more quickly.

“There is a strong case for the MPC to help boost bank lending to businesses by immediately raising its purchases of private sector assets. For QE to be truly effective, it is critical that the additional funds should urgently go into the real economy. The Committee should also impose negative interest rates on deposits held by commercial banks at the Bank of England, which could help to boost the availability of credit.

“By confirming that interest rates will not be raised until the end of 2012, as the Fed has done in the US, the MPC can help to underpin business confidence. We appreciate that the MPC must be concerned over above-target inflation, but this is likely to fall next year, while the threats to growth are more serious at the present time.”

Graeme Leach, chief economist at the Institute of Directors:

“What did we want? More QE. When did we want it? Now. Near zero GDP and money supply growth made a compelling case and the Bank of England was right to launch QE2. It could be argued that the Bank of England was slow to introduce QE the first time, but thankfully it hasn’t made the same mistake twice.”

The CBI today responded to the announcement from the Bank of England’s Monetary Policy Committee (MPC) that it will extend the Asset Purchase Programme.

Ian McCafferty, CBI Chief Economic Adviser:

“With the risks to the economic outlook increasing, the MPC has acted promptly by extending quantitative easing this month.

“This measure will help support confidence, but we need to recognise that its impact on near term growth prospects is likely to be relatively modest. Only once the turmoil in the Eurozone

is resolved will confidence be fully restored.”

Andrew Smith, KPMG’s Chief Economist:

“Now the MPC has decided that the weak economy warrants another round of QE, it is likely to prove just the first instalment of a larger injection. With the government still intent on rapid deficit reduction, consumers constrained by shrinking real incomes and our major export markets experiencing similar headwinds, a sizeable monetary expansion may be the only instrument available to support demand for the foreseeable future.”

Stephanie Flanders, Economics Editor, BBC:

The US comedian, Mitch Hedberg, had a line I reprised on the Today programme this morning: “My fake flowers died, because I forgot to pretend to water them.”

There’s something of that in the city’s support for QE2. It may not do a huge amount of good, but it could seriously hit confidence if the Bank seemed to have nothing left to throw at the recovery.

On this view, the Bank needs to pretend to water the economy, even if there’s less and less chance of it doing any good.

Tom Clougherty, executive director of the Adam Smith Institute:

More quantitative easing means more kicking the can down the road. It means preventing markets from adjusting, and it means perpetuating the misallocated capital, excessive risk-taking, and over-leveraged balance sheets that got us into this mess in the first place. To put it simply, printing money does nothing to solve our current problems. If anything, it makes them worse.

There will be no return to sustainable economic growth until the authorities realize that we can’t defy economic gravity forever. Recessions are about adjustment and recalculation, and as long as policy is designed to prevent the liquidation of bad investments, the paying down of debt, and the reallocation of scarce economic resources, recovery will remain elusive.

Here are the economic policies we need: an effective bank resolution regime, a stable monetary environment, and a thoroughgoing commitment to removing tax and regulatory barriers to investment and entrepreneurship. Right now, we aren’t getting any of them.

Jeremy Warner, assistant editor of The Daily Telegraph:

But I worry about it[Monetary Policy Committee’s decision to increase “quantitative easing” by a further £75bn]. I worry both that it will be ineffective in terms of stimulating investment and growth, I worry that it is going to be very difficult for the Bank of England to unwind these now vast holdings of government debt, I worry that we are now perilously close to outright monetisation of the deficit (a policy approach which all economic history shows ends in abject disaster), and I worry that ultimately, it’s bound to be inflationary.

Allister Heath, editor City A.M (tweeting):

“UK QE today was at the very least premature. Nonsense to claim that without it we would face deflation. Not sure how will help Euro crisis.”

Faisal Islam, Economics Editor, C4 News (tweeting):

“Woahhh! £75bn of QE…”

“Mervyn’s magic money merrygoround rides again. £75bn. Bigger and earlier than markets expected…”

“Is there any point having an inflation target?”

“It’s plan BoE …”

“Gilt yields already at record lows pre-QE… Economy flat. So will pushing them down even further really make a difference?”

Pension funds called for an urgent meeting with the Pensions Regulator yesterday to discuss ways of protecting UK pensions from the negative effects of quantitative easing.

Joanne Segars, Chief Executive at the National Association of Pension Funds (NAPF):

“A strong and growing economy is essential for the long-term sustainability of UK pensions. Quantitative Easing is a price worth paying, but only if it is successful in delivering the growth that businesses and pension funds need.

“But this measure has adverse consequences for pension funds in the short-term. Quantitative Easing makes it more expensive for employers to provide pensions, and will weaken the funding of schemes as their deficits increase. All this will put additional pressure on employers at a time when they are facing a bleak economic situation.”

Joanne Segars added:

“It is crucial that the Pensions Regulator takes into account the negative impact of Quantitative Easing on pension schemes. Lower interest rates will increase pension deficits, making them look artificially large. This is even more worrying as the Bank of England is intending to extend its gilt purchases into longer term maturities, which will have a larger impact on pension fund deficits.

“We are writing to the Pensions Regulator to request an urgent meeting to discuss the implications of Quantitative Easing on pension funds and what can be done to protect them.”

Adrian Coles, Director General of the Building Societies Association:

“With the economic recovery weakening, the expansion of quantitative easing is not unexpected. The additional asset purchases of £75 billion announced today by the MPC will inject money into the economy, which will hopefully feed through to bolster demand. If successful this should then support confidence, potentially leading to an increase in savings. This in turn creates a better environment in which mutuals can lend.”

What will QE mean for the economy, and for you? Have your say below.

Leave a Comment