Today saw the European Central Bank (ECB) announce its final interest rate decision of the year, keeping current rates in place, as markets had expected.

While the central bank does not expect inflation to reach its target before the year 2025, it reiterated the upward risks of inflation that may come as a result of the high cost of labor.

The following press release appears to have contributed to strengthening the markets’ hope about an interest rate cut next year, which pushed the euro to rise to its highest levels this month against the dollar, reaching 1.09335, which is located a little close to the highest levels this month that we also witnessed today, in addition to regain of losses for German bond yield, after sharp declines this week, reaching 2.130%.

With the chapter on the current year closed, the narrative now moves from the end of the interest rate hike cycle to the expectations about when and how much the ECB will cut next year.

While this decision will never be easy for monetary policy makers, given the number of contradictory factors that may make them face the risks of reigniting inflation or pushing the economy towards further decline.

On the one hand, inflation continues to decline further, sometimes more than expected, heading towards its target of 2%. Last November, annual inflation fell to 2.4% and core inflation to 3.6%, the lowest levels since July 2021 and April 2022, respectively.

In addition, the Producer Price Index (PPI) continues its steepest decline in history during the three months ending in October, with a decline of 12.4% year-on-year in September.

On the other hand, many monetary policy makers still fear that progress in combating inflation is not enough and also fear an interest rate cut at a time when the upside risks to inflation are still intact.

These fears of a return to high inflation come either from the steps that oil-exporting countries may take to support relatively low oil prices or from the supply constraints and disruption to supply chains that may be caused by the conflict in the Middle East emerging from its current scope or extreme natural phenomena, this is what Christine Lagarde talked about in the press release as well.

Not only that, as the market’s extreme optimism regarding an interest rate cut next year, which has reached 150 basis points, may also hamper the efforts to reduce inflation.

This is because these expectations push bond yields towards further declines, which in turn may push borrowing costs to decline, which may stimulate economic activity in a way that decision makers may not want. For example, German 10-year bond yields are at their lowest levels in a year.

This is what may prompt central bank officials to avoid direct talk about any interest rate cut next year and to continue talking about hiking it if necessary.

The labor market also appears to remain solid which may encourage the ECB to keep rates high. This is because the unemployment rate is still at its lowest historical level since the establishment of the Eurozone at 6.5%, and the annual rate of wage growth is still relatively high at 4.6% despite the decline in the previous two months.

However, maintaining interest rates at their record high levels comes with a further decline in economic activities, which are still recording contraction, and a relatively low level of sentiment about the possibility of restoring growth soon.

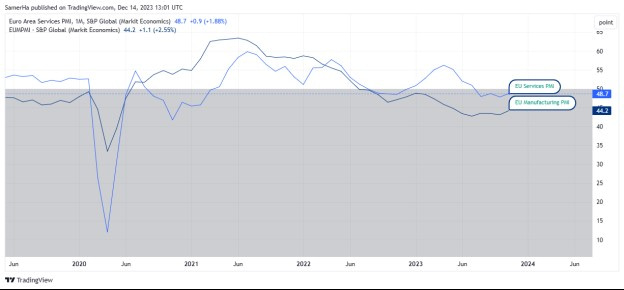

As service activities are still contracting since last August, and manufacturing activities are continuing to contract since August of last year, according to the Purchasing Managers’ Index for both sectors from S&P Global.

Eurozone services and manufacturing PMI. Source: TradingView

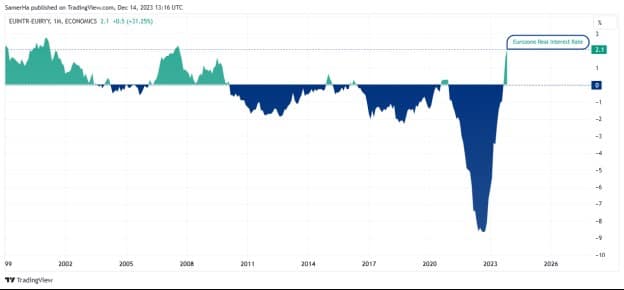

Also, keeping interest rates high in conjunction with the continuing trend of declining inflation may push real interest rates to rise further as the impact of lagging monetary tightening measures, which may put more pressure on the lost economic growth.

This is because higher real rates may lead to more high borrowing costs in conjunction with a greater tendency toward saving. While real interest rates are already at the highest levels since 2007 at 2.1%.

Real interest rates in the euro area. Source: TradingView

The good thing is the continued confidence in the ability of the region’s economy to stop deflation and restore growth, even they still relatively low, according to recent surveys of Eurozone investors, in addition to the continued resilience in the labor market, as we mentioned above, which is what monetary policy officials praise for its role in maintaining financial and banking stability.

Leave a Comment