The impact of the COVID-19 pandemic on tax revenues was less pronounced than during previous crises, in part due to government support measures introduced to support households and businesses, according to new OECD research published today.

The 2021 edition of the OECD’s annual Revenue Statistics publication shows that the OECD average tax-to-GDP ratio has risen slightly to 33.5% in 2020, an increase of 0.1 percentage points since 2019. Although nominal tax revenues fell in most OECD countries, the falls in countries’ GDP were often greater, resulting in a small increase in the average tax-to-GDP ratio.

This year’s edition includes the first comparable analysis on the initial tax revenue impacts of COVID-19 across OECD countries, which suggests that government support measures contributed to the relative stability of tax revenues by protecting employment and reducing corporate bankruptcies to a considerably greater extent than in the global financial crisis in 2008-2009.

The report also finds that many of the tax policy measures implemented to support households and businesses often had a direct revenue cost via reductions in tax liabilities, enhanced tax credits and allowances and reductions in tax rates. The sharp reduction in economic activity in 2020 reduced labour force participation, household consumption and business profits, further affecting tax revenues, although the shock was shorter and more sector-specific than the global financial crisis, contributing to its more muted impact on tax revenues.

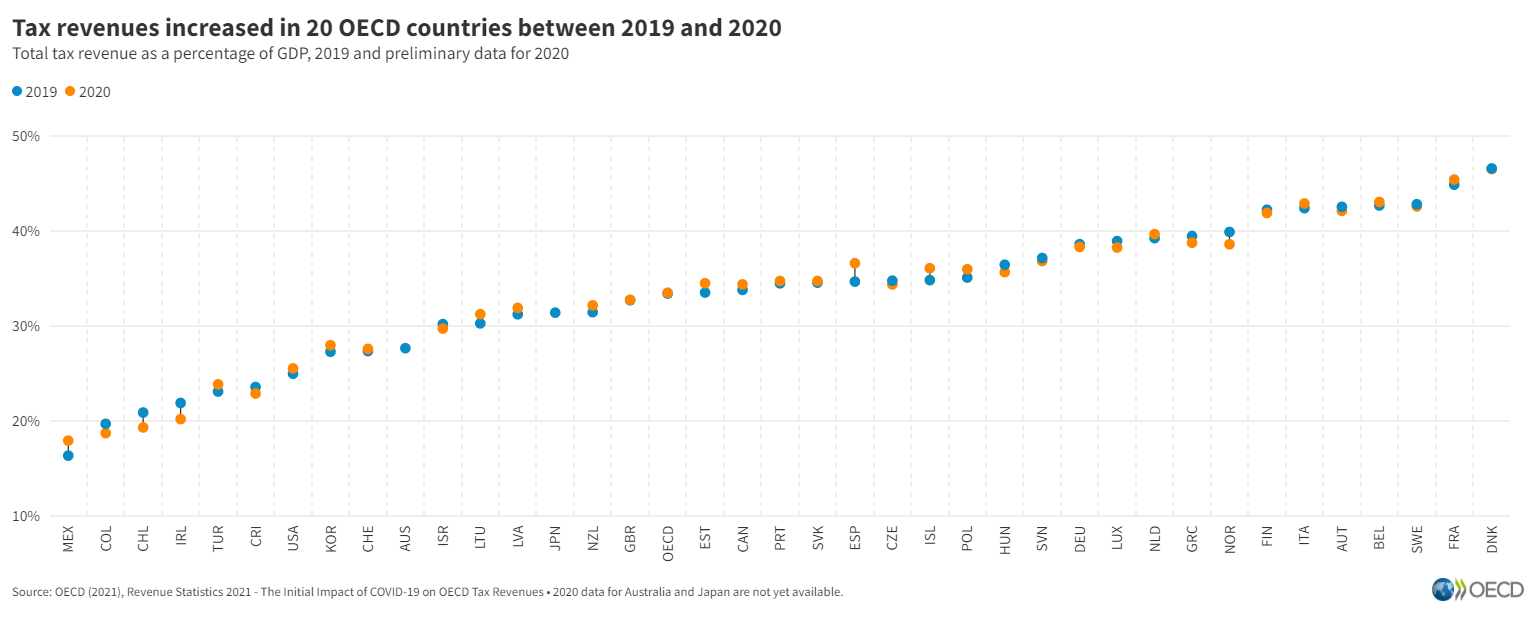

The report shows that countries’ tax-to-GDP ratios in 2020 ranged from 17.9% in Mexico to 46.5% in Denmark, with increases seen in 20 countries and decreases in the other 16 for which 2020 data were available. The largest increases in tax-to-GDP ratios in 2020 were seen in Spain (1.9 percentage points), which experienced the largest fall in nominal GDP and a lower fall in nominal tax revenues.

Other large increases were seen in Mexico (1.6 p.p.) and Iceland (1.3 p.p.). The largest decreases were seen in Ireland (1.7 p.p.), partially due to lower VAT revenues following a temporary reduction in VAT and decreased economic activity. Other large decreases were seen in Chile (1.6 p.p.) and Norway (1.3 p.p.). In Norway, the fall was due to a sharp decrease in corporate income tax revenues due to temporary changes in the Petroleum Tax Act during the pandemic.

Across the OECD, corporate income tax and excise tax revenues were the most negatively affected by the COVID-19 crisis. Corporate income tax revenues saw the largest average decrease (0.4 p.p. of GDP, with declines in 26 countries); and lower fuel use due to mobility restrictions led to a small but widespread decrease for excise revenues (0.1 p.p. on average with declines in 28 countries).

By contrast, personal income taxes and social security contributions saw an increase in revenues, on average (by 0.3 p.p. in both cases, and in 28 and 29 countries respectively). The fact that revenues from these two taxes held up most likely reflects that governments provided considerable support to maintaining the connection between workers and the labour market in this crisis. No change was seen in property taxes or VAT as a share of GDP, on average.

Leave a Comment